Should You Offer “Buy Now, Pay Later” Options on Your eCommerce Website?

Installment payments aren't new - layaway plans have been around forever. But "Buy Now, Pay Later" (BNPL) services like Affirm and Afterpay have put a digital spin on installment financing in the world of online shopping.

I took notice when BNPL options started proliferating across checkout pages. These services promise higher conversion rates and order values. Flexible financing is clearly enticing for shoppers seeking to avoid credit card debt.

Still, I wondered if BNPL delivers everything it claims for merchants. Is it really a miracle conversion booster, or a potential consumer debt trap? I suspect the truth lies somewhere in between.

I was mulling this over while listening to Marketplace on NPR the other day. They featured a segment on BNPL and the growing popularity of deferred payment services. It got me thinking we should dig deeper into the merchant side of things.

In this post, we’ll explore how BNPL actually works and break down potential upsides and drawbacks for eComm shops. My goal is to arm you with enough info to decide if BNPL deserves a spot at your checkout. Sound good? Alright, let's get into it - but first here’s that little audio snippet if you’d like to check it out for yourself:

They begin, of course, by stating the obvious; which in this case is the fact that the pandemic drove everyone to online shopping like never before. If you’re one of those people, you’ve most likely noticed a few new payment options popping up everywhere online. And these aren’t just the normal “alternate” ways to pay like Apple Pay or Google Pay. These new offerings offer financing and payment plans in addition to traditional payments run through a merchant payment processor like Stripe or Paypal.

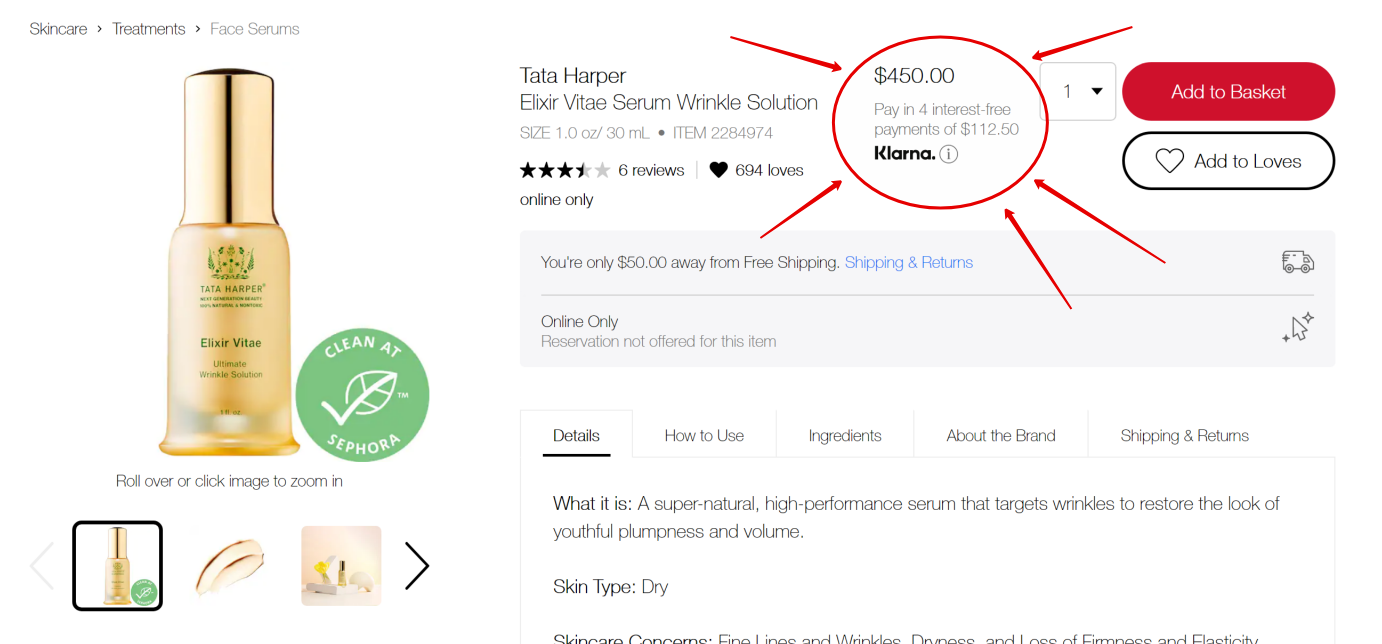

Here’s one of my faves, Sephora - letting me know that this $450 wrinkle serum can be mine for 4 easy payments of just $122.50!

Here’s Anthropologie encouraging me to buy this super cozy looking blanket at the low, low price of just 4 interest free payments of $37.

And it’s not just luxury or premium brands getting in on the action. Here’s Walmart letting me know that this super big TV can show up at my door for just $74/mo. It’s enough to make you want to sort prices from high to low, right?

This Ain’t Your Grandma’s Layaway Plan

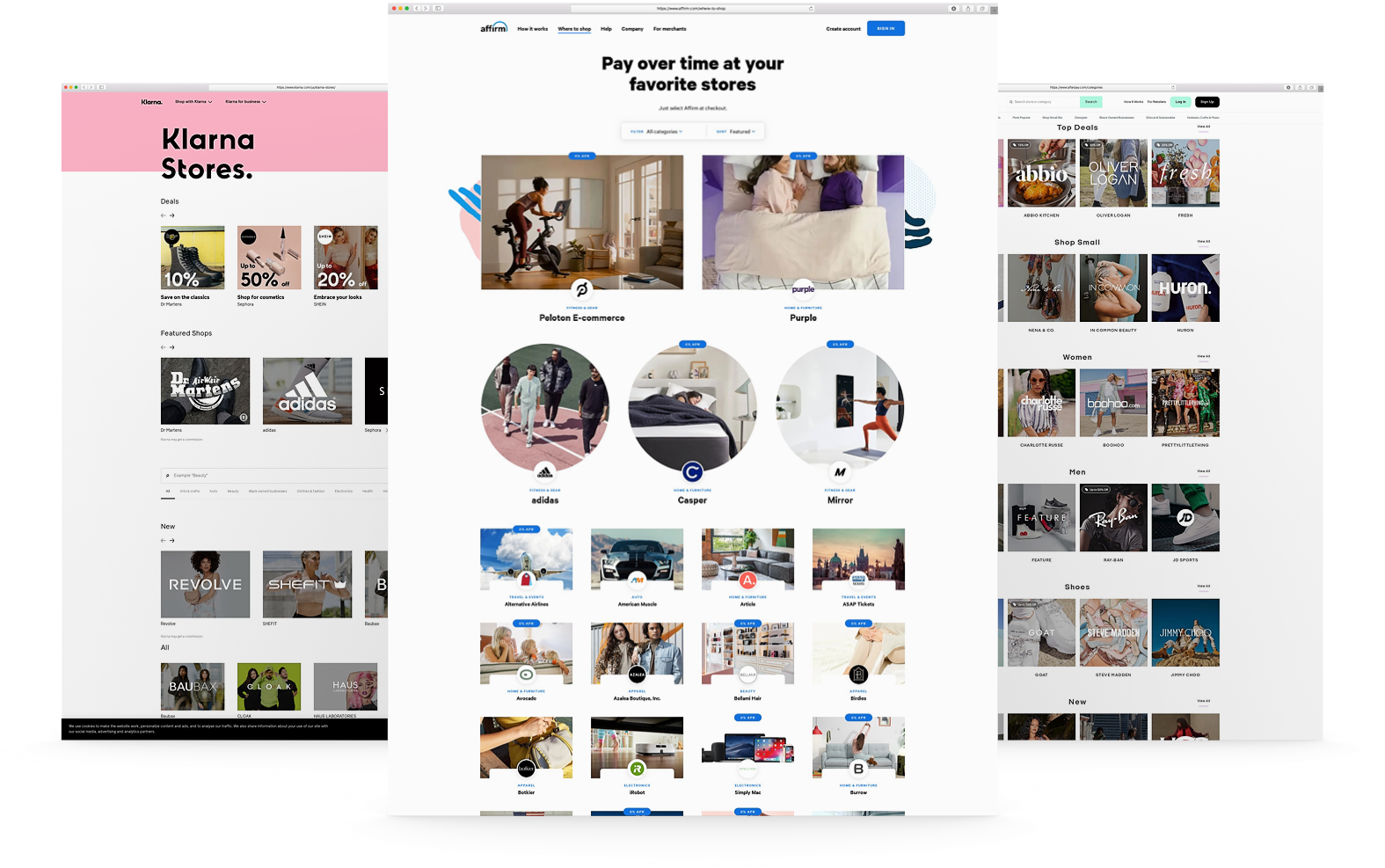

Online sellers of all sizes are turning to services like Klarna, Afterpay, Affirm, and others to offer financing for purchases big and small. Payment plans are obviously nothing new but unlike old school layaway plans where the retailer held the item until it was paid in full, in this case, people can check out and receive their orders on the promise of making their monthly payments to the company the merchant has partnered with.

The idea of merchant-side financing also isn’t exactly new. Home shopping networks like QVC and HSN have offered things like “Easy Pay” and “Flex Pay”, respectively, for a while. They were early adopters of the idea that there are profits to be had if you make it as easy as humanly possible for people to buy from you, and reduce any and all friction in the process - even if that’s financial friction.

When it comes to eCommerce, my friends at NPR pointed out that payment plans like these are especially popular amongst younger shoppers who are leary of amassing credit card debt. This doesn’t mean that the arrangement is without some risk to the consumer… and some cost to the seller. So, what are the benefits and drawbacks? Let’s dig in!

How It Works

Whether you call it financing, “Buy Now, Pay Later” or payment plans, all of the services pretty much work like this:

Customer Side

Shop like normal. At checkout, select the alternative payment method and sign up for an account with the provider (i.e. Klarna, Afterpay, Affirm, etc.). Make the regular payments as agreed directly to the payment service provider.

Merchant Side

Orders come in and are fulfilled like normal. You’re paid in full, less the processing fee charged by the payment service provider. They’re basically stepping in as the middle man, offering to pay you now while they get paid overtime.

By The Numbers

All of the various companies have different stats to promote their services but when I dug into the numbers offered up by all of them and compared them, there were some definite commonalities.

Adding an alternate payment method:

Increases average order value

Increases conversion rates, especially amongst first-time visitors

Boosts repeat visits

Reduces cart abandonment

Reduces return rates

Another hidden perk offered by pretty much all of the companies doing this right now is that your brand will automatically show up on their list of merchants, right alongside other big names who use the same service. This can be a huge way to get noticed by fresh eyes and help you get some traction if you’re on the smaller side or your brand is completely new.

What’s the catch?

If you’re thinking that all of this seems too good to be true, you’re only partly right. In the NPR story, they reported that it’s easy for some consumers to get in over their head on payment plans and, of course, if payments are missed there are financial ramifications. At least one of the providers, Affirm, does tout that although applying does require a quick credit check to determine eligibility that this won’t negatively impact the shopper’s credit score and that on time payments can actually help them boost their rating.

Merchants will also see higher merchant fees charged on orders that used the financing gateway to checkout, though payment service providers are also quick to point out that increased cart values, higher conversion rates and lower return costs among other benefits all offset the small percentage they charge over traditional merchant processors. And, in case you’re wondering, that extra percentage will vary but is between 2% and 6% on average.

Should You Do This?

In short, my answer is yes. Here’s why. Even though you will pay more in merchant fees for each order where the customers select this option you have to keep the following things in mind:

Just because you offer financing as an option, doesn’t mean everyone will take it. The people who were going to buy from you anyways will still use their credit cards like normal.

A percentage of something is better than a fraction of nothing. The people who weren’t going to buy from you but needed this as a little incentive are all incremental sales.

It can make you look bigger and more established if you’re a new or smaller brand. Think of the sales pages and apps offered by financing providers as another sales channel. The percentage you pay to them is just your entrance fee to be listed on their pages. New fans may come to you through those pages but then become fans that buy from you again and again! (If this resonates with you, you may also like this post on how your small business can compete with Amazon on shipping.)

If you’re not sure, I would say there’s nothing to lose by adding a “Buy Now, Pay Later” option and just see how it resonates with your fans. You can always decide later that it’s not for you or if this fad fades out just turn it off. My guess is that it won’t, but - hey, just know you have the option!

For instructions on how to add Afterpay to Squarespace, check out this post!